The first two points are likely to be part of the wider internal discussion on CSRD compliance. However, they may have a specific impact in the context of disclosures your company is required to make in a capital markets transaction. The last three developments are specific to the transactional process you will go through in an equity or debt capital markets transaction. Although similar to what you may see in an M&A process, each of these issues has its own nuances in the capital markets context.

-

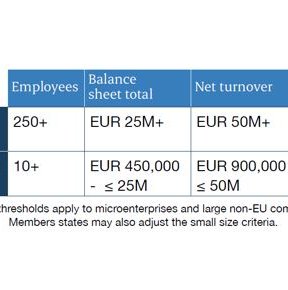

1. Know when your company has to start reporting under the CSRD

From 2024, the Corporate Sustainability Reporting Directive (CSRD) will apply to public interest entities (including listed companies) with more than 500 employees and/or EUR 50 million turnover and/or EUR 25 million balance sheet total. The Accounting Directive has recently been amended to adjust the monetary size criteria of the CSRD (balance sheet and net turnover) for micro, small, medium-sized and large companies by 25%. As shown in the table below, more companies will fall within the scope of the CSRD in each of the coming years.

Once the CSRD applies, the company’s management report will have to include information on various sustainability topics. To name a few, it will need to include time-bound sustainability targets, the role of the management and supervisory bodies in relation to sustainability matters, a description of the business model and strategies, including resilience to sustainability risks, sustainability opportunities, implementation of actions in line with the Paris Agreement, sustainability-related management incentive schemes and risks, and actual or potential impacts related to the company’s own operations and those of its value chain. This brief description illustrates the impact and diversity of disclosures in the management report.

All disclosures made in the management report must be consistent with the disclosures made at the time of a capital markets transaction. This applies whether a prospectus is required or whether the transaction is undocumented. Information that is no longer accurate at that time, for example because a target has not been met, must be publicly amended.

Taking this a step further, the latest draft of the Listing Act, which is expected to come into force later this year, states that the management report must be incorporated by reference into any prospectus for the listing of securities on a regulated market. This means that any management report as published in the year(s) immediately preceding a prospectus will be directly subject to the relevant prospectus liability regime. If you are contemplating a capital markets transaction that may require a prospectus, such as an IPO or a bond issue on a regulated market, it makes sense to take this into account when preparing the company's current management report.

Finally, we expect to see a group of companies preparing for an IPO in 2024/2025 before they have had to publish CSRD-compliant management reports. These companies should think of the engagement with the regulator as an opportunity to get their disclosure right. If approached correctly, it can be beneficial.

-

2. Understand the internal controls needed to comply with the CSRD

A key part of CSRD compliance will be to ensure that the company has internal controls in place to source and evaluate relevant data. If the company anticipates serious gaps in its internal controls, this would be disclosable in a prospectus. Investors may view this as a serious risk and we would expect the existence and robustness of the internal controls to be probed by them or the advising banks. For example, there is no grace period for newly listed companies to put in place the internal controls necessary to comply with the CSRD. In anticipation of a capital market transaction, it is therefore important to have had an internal discussion and to have a clear view on the existence and robustness of internal controls in order to comply with the CSRD.

During the review period of a prospectus, it is expected that the regulator may ask questions about sustainability reporting. These may be direct questions about internal controls or about the reported information itself. A tight timetable will often be agreed with the regulator. This will include windows during which the regulator can comment on the disclosure in the prospectus and when it expects answers to its questions. In order not to delay the transaction or the prospectus process, it is useful to ensure that the right people in the company who are responsible for - or have been involved in - obtaining and interpreting the sustainability data are available to answer the regulator’s questions.

-

3. Be aware of ESG targets that you want to report on and their impact on future disclosures

The CSRD requires certain targets to be set out in the management report, for example on green house emissions. However, in the current climate, businesses may also very much be tempted to set their own targets for commercial reasons or reasons of attracting investment. Many companies considering an IPO are growth companies. When setting targets today, please consider whether they are phrased in a way that still works if you indeed meet your growth targets. For example, when setting targets to reduce the use of packaging materials, consider whether these are best expressed in terms of absolute numbers, percentages compared to current use, or percentages of overall use.

A similar approach can be taken for corporate governance ambitions, such as those related to diversity or remuneration. Which of the goals are likely to grow with you, and which goals may be realistically unattainable as you grow? In a capital markets setting, you will be forced to scrutinise your targets and adjust them publicly if necessary. Think carefully when setting your targets from the get-go to avoid what may be a normal consequence of growth but may look like a missed target.

-

4. Are you likely to need a prospectus for your capital markets deal? Check potential areas of impact on prospectus disclosure

The Prospectus Regulation sets out in detail what must be included in a prospectus. Chapters typically have standard headings and investors and regulators expect to see certain information in a particular order. Looking at what is already required, there are a number of areas where sustainability reporting can have an impact on disclosures. Examples include what is said about sustainability in the ‘strengths and strategy’ sections of a prospectus (both proactively and as part of the cost of compliance). If the proceeds of the transaction are used to meet ESG objectives, this will lead to additional disclosure and scrutiny of the ‘use of proceeds’ section. In particular, in IPO or other equity prospectuses, the company sets out certain areas including strengths and strategy. The parts of the prospectus describing the company's industry may require additional attention due to the ESG risks faced by that industry in general.

Risks and mitigating factors required to be disclosed in the management report under the CSRD must be included in the prospectus. However, risks may need to be separated from mitigating factors in line with the rules for risk factors in the prospectus. If management remuneration is linked to ESG goals, this may also lead to additional disclosure in the prospectus. These are just some examples. Once we understand your industry and business, we can provide a more complete analysis of the impact of your ESG disclosures on the prospectus. We can provide you with an overview of the areas to consider disclosure for that are relevant to your business in the context of a capital markets transaction.

-

5. Be ready to incorporate ESG into any capital markets due diligence process

If you are considering a capital markets transaction, you are probably also preparing for a due diligence process. If you are required to make ESG disclosures, or are making them on a voluntary basis, be prepared for banks and investors to want to verify your statements. Ensure that you have sufficient verification material for key issues such as ESG risks, the impact on the company’s strengths and strategy, and any stated targets.

Similarly, market parties may want to understand what the company will report on going forward in relation to ESG and whether internal controls are in place to collect and verify the data underlying the claims that the company will report on. In addition to this more practical approach, the Corporate Due Diligence Directive (CSDDD) will require listed companies or bond issuers to implement a mandatory human rights and environmental due diligence process in future (see our CSDDD update for more information).

-

How we can help

We are happy to discuss how the CSRD may affect your company and capital market transactions. We can help you understand the prospectus process, areas of regulatory scrutiny, and time-sensitive information. We can also help you consider whether preferred phrasing of ESG targets and governance may be more or less scrutinised in the context of a capital markets transaction, and advise you on what information to provide for ESG due diligence and how to prepare for the CSDDD. Sign up for our monthly ESG Matters Update to keep abreast of the latest developments in ESG governance, disclosure and litigation.

-

Download

For the PDF, click here